If you are not a resident of the United States of America who does work or earns income in the USA or by foreign business entities— then you will encounter W8-Forms submission.

The W8-BEN form is called the— “Certificate of Foreign Status of Beneficial for United States Tax Withholding.” In simple terms, the W8-BEN form is a legal tax document required by the IRS or the Internal Revenue Service in the United States of America in order to declare your tax status.

As a non-resident, you may find it a complicated process to complete the W8-BEN form. We are, nevertheless, available to assist you in comprehending the W8-BEN form and ensuring a smooth submission process. Let’s check the table of content to see what you’ll cover ahead:

- Understanding Form W8-BEN

- Purpose of Form W8-BEN

- Significance of W8-BEN

- Who Needs to File a W8-BEN form?

- How do I File a W8-BEN form?

- Difference between W-8 forms and W8-BEN

- Step-by-Step Guidelines for Completing the W8-BEN

- Where should the finished W8-BEN form be sent by the contractor?

- Countries that have Tax Treaties With the United States

- Frequently Asked Questions (FAQs) Associated with W8-BEN

- How Deskera Can Assist You?

Let’s Dive in!

Understanding Form W8-BEN

W8-BEN or W8 forms are Internal Revenue Service (IRS) paperwork used by foreign firms and non-resident aliens (NRAs) to authenticate their country of residency for tax purposes, verifying that they claim for a lower tax rate withholding.

Depending on the nature of income, foreign people who received income from a US source are liable to a 30 percent tax withholding rate.

W-8 forms are issued by the IRS. However, they are only delivered to withholding agents or payers, not to the IRS.

Note: If you are a legal citizen of the United States then you will never have to bother about filling out the form. Foreign persons or businesses must use these tax forms to establish their foreign status.

Purpose of Form W8-BEN

FORM W-8BEN will assess whether you are entitled to treaty benefits. The goal of the form is to determine:

- The person is a foreign national (legally a non-resident alien) who is not a citizen of the United States.

- The individual in question is the beneficial owner of the Form W-8BEN-related income.

- Because of an income taxation agreement between his home country and the United States, the individual is entitled to a reduced rate of tax withholding or is completely exempt.

Moreover, to be in the accordance with the existing regulations and rules of the IRS, you must issue Form 1099 to your independent employers.

These employers or contractors could be the citizens of the United States (even if they live overseas) or who live in the United States and have the legal right to work and live here.

If you recruited someone from another nation to conduct services for your firm. Then, you don’t have to particularly send them the form 1099 at the end of the year if your contractor is based in another nation and does not conduct business in the United States.

Moreover, it is critical that you must keep records proving that your contractor is not a U.S. citizen or resident, as a result, shouldn't be issued end-of-year forms (such as 1099s) or liable to withholding tax.

And that's where the W8-BEN comes into the picture.

To assure that your company is in compliance, you must request a filled Form W8-BEN from a foreign contractor.

The W-8BEN is used to prove that your contractor is a foreign person who, if eligible, can seek a reduced rate or exemption from income tax withholding as a resident of another nation.

This form can also be used to establish a person's Chapter 3 or 4 status in order to avoid paying taxes on certain types of income, such as

- Dividends;

- Rents;

- Interest (including certain original issue discount (OID));

- Compensation for services performed…and more

Note: Form W-8BEN should only be used by non-US citizens. Forms W-9, W-4, and others are filed by citizens of the United States.

Significance of W8-BEN

The W8-BEN is used to determine whether or not someone is a foreign national (certificate of foreign status).

Furthermore, W8-BEN forms are used to support a 30% tax rate during audits. In addition, it helps to claim that a non-resident alien (NRA) is the beneficial owner of the revenue for which Form W-8BEN is being submitted.

If you are a foreign contractor or employee, you must report all foreign income generated in the United States on your taxes. If you reside in a foreign country with which the US has an income tax agreement, completing Form W-8BEN could result in a lower withholding rate or possibly a complete exemption from the withholding tax.

It's critical to complete the form as quickly as possible because the treaty prohibits you from being taxed twice (once by the US government and again by your home government).

Who Needs to File a W8-BEN form?

A nonresident alien who has earned income that would usually be subject to tax withholdings in the United States must fill out the W8-BEN form.

To put it another way, it is performed by the foreign worker, not by the USA businesses or employers. Furthermore, this form should not be filled out by foreign businesses or intermediaries.

In most cases, Form W-8BEN is only completed when the withholding agent, payer, or foreign financial institution requests it. Moreover, it becomes effective on the date it is signed and expires on the final day of the third calendar year after that.

However, if circumstances change and the records on the form become inaccurate, a new form must be completed within 30 days. A change of circumstances could be a move to the United States or to another foreign country.

Following we have listed when not to use Form8-BEN. Check out to avoid any confusion:

How do I File a W8-BEN Form?

According to the IRS Instructions for Form W8-BEN, "You must notify the withholding agency, payer, or FFI with which you have an account within 30 days of the change in circumstances and file a new Form W-8BEN or other applicable form,"

Make sure that you send the completed form to the entity or party who requested it. Also, do not submit the form W8-BEN to the Internal Revenue Service (IRS) or include it with your tax return.

Furthermore, this party or entity is usually the individual or organization from whom you received pay.

The withholding agency may be compelled to withhold the full 30% needed by US tax law if the tax documents are not submitted before the first payment is received.

The W-8BEN form will be valid for a period of three years. A Form W-8BEN is valid for three full calendar years after it is completed.

However, if your circumstances change and the information on a previously filed W-8BEN is erroneous, you must file a new W-8BEN as soon as possible.

Difference between W-8 forms and W8-BEN

W-8 forms come in a variety of formats, which can be bewildering. Here's a basic rundown of the W-8 family of forms:

Step-by-Step Guidelines for Completing the W8-BEN

All of the Internal Revenue Service's forms and instructions, along with the W-8BEN form and Directions for Form W-8BEN, are available at www.irs.gov, America's tax authority.

Following we have discussed step-by-step directions that will help you to easily complete the W8-BEN form. The W8-BEN form is divided into three main parts. Let's learn:

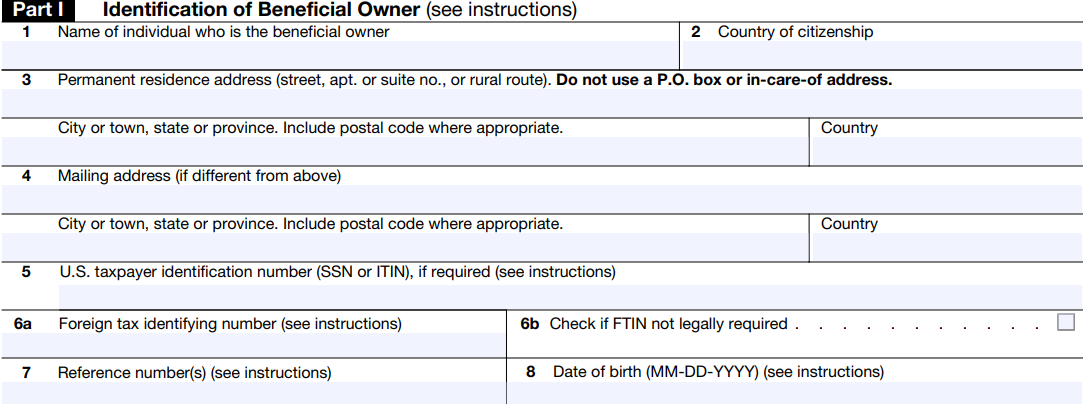

Filing Part I: Identification of Beneficial Owner

Check part 1 of the form:

Line 1: The beneficial owner's name is requested on this line of the form. This is the name of the individual who is completing out the form: this is the foreign worker who has been paid by an American.

Line 2: The citizenship country is requested on the section 2. Input the country where the contractor is both a citizen and a resident if the contractor is a dual citizen.

Even if the contractor has dual citizenship in another jurisdiction, U.S. residents or resident aliens will very certainly be required to file form W-9 instead. The W8-BEN is usually only filled out by those who are not citizens or residents of the United States.

There's even more tiny print on this one, which contains single-owner organizations that aren't counted. To guarantee compliance, those completing out this form should consult with a CPA.

Line 3: The permanent residence address is listed on line 3 and includes the city, town, state, province, postal code, and country. A PO Box, a financial institution, or care of address should not be used when filling out the form.

Line 4: The mailing address is on line 4. Only fill this area if the mailing address differs from the permanent residential address indicated above.

Line 5: If the contractor is a resident alien, line 5 demands the contractor's U.S. taxpayer identification number, that could be individual tax identification number or social security number. If the contractor is seeking treaty benefits and/or a reduced withholding rate, he or she must supply an SSN or TIN.

Line 6: On the line 6, you'll be asked for a foreign tax identification number.

Line 7: Line 7 asks for the withholding agent's reference number. The number of the account to which transactions are being made may be included by the contractor. In some situations, the withholding agent will file this line to refer to a specific account or form which should be linked with this W8-BEN.

Line 8: The contractor's date of birth is requested on line 8. As noted, this should be stated in the month-day-year format ((this is unfamiliar for residents or citizens of other nations, because the month-day order is frequently flipped outside the United States.))

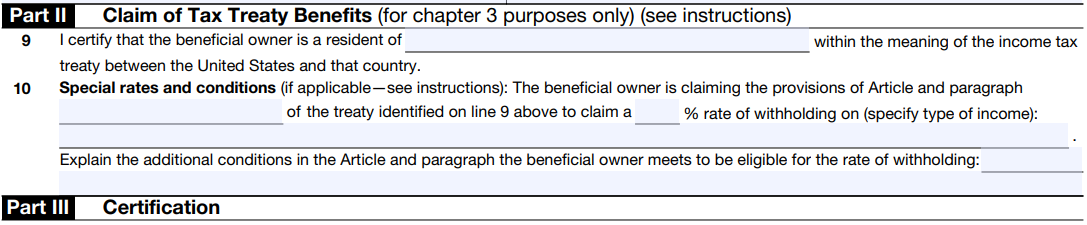

Filing Part II: Claim of Tax Treaty Benefits

Only use this section if the contractor is seeking treaty benefits as a citizen of a foreign country with which the US has an income tax treaty under Chapter 3 of the Internal Revenue Code (withholding of tax on non-resident aliens and foreign businesses).

Line 9: It verifies that the contractor's home country has a tax agreement with the US in this section.

Line 10: Line 10 is reserved for unique withholding tax rates or conditions between the United States and the resident countries, as well as a blank line for any additional remarks or explanations of qualifying for the special rate.

You may see a current list of these tax treaties here.

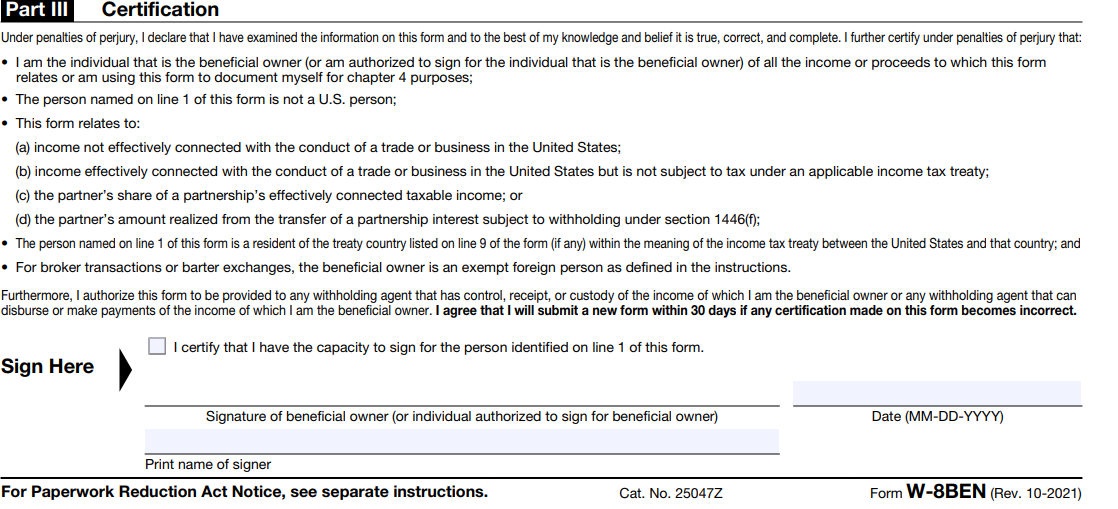

Filing Part III: Certification

This is the area where the foreign contractor (or an authorized person) signs and verifies that they are not a U.S. person and that the revenue reported on this form was not earned or related to a business in the United States.

Moreover, it certifies that the income is not subject to withholding tax or taxation at a higher rate and that the contractor promises to file a fresh form within 30 days if any material on the document becomes inaccurate.

Finally, the paperwork should be signed and dated by the contractor.

Where should the finished W8-BEN form be sent by the contractor?

The contractor must not send the paperwork to the IRS once it is completed. The form should instead be delivered to you, the employer. Remind your contractor that the form includes sensitive information, so make sure you deliver it safely.

If your contractor has given you a completed W8-BEN, it's vital that you protect the information as carefully as you would any other valuable document.

Countries that have Tax Treaties With the United States

The U.S.A is in taxation agreement with certain countries. Residents of qualified foreign nations (who are not generally citizens of those countries) may be qualified for reduced tax rates on U.S. sources of income under these agreements.

The following nations have tax treaties with the United States:

Furthermore, earners of qualifying income must take out Form W-8BEN to establish a claim for tax treaty advantages under the Internal Revenue Code. The Internal Revenue Service's website has a complete list of treaty countries.

Frequently Asked Questions (FAQs) Associated with W-8BEN

Following we have discussed some crucial frequently asked questions (faqs) associated with W-8BEN forms. Let’s learn:

Que 1: What happens if the W-8BEN isn't carried out correctly?

Ans: The foreign person may be subject to federal tax withholding of 30% if the paperwork is not completed correctly.

Que 2: What about the expiration of Form W-8BEN?

A Form W-8BEN is generally valid for three years. It further commences on the date it is signed and ends on the last day of the third calendar year once it's been completed unless there is a change in circumstances that causes any material on the form to be incorrect.

Que 3: What is the procedure for obtaining my W-8BEN?

The organization making the payment to the person sends Form W-8BEN. The IRS, not the corporation or entity who sent form W-8BEN, should receive the form.

Moreover, it's also not intended to be submitted along with a tax return. The paperwork should be filed before the first payment is received, in most cases.

Que 4: What is the function of a W-8BEN-E?

Unlike the W-8BEN, which is only for people, the W-8BEN-E is for businesses.

Moreover, the W-8BEN-E is essential because foreign corporations are entitled to the same 30% withholding tax rate as individuals.

Businesses, like individuals, may, nevertheless, be eligible for a lower tax rate. The W-8BEN-E is a form that aids in determining eligibility for reduced rates.

Que 5: What types of earnings are entitled to 30% withholding but aren't reported on Form W-8BEN?

Certain forms of income produced in the United States will be exempt from the 30% withholding tax. These sorts of earnings include:

- Short-term (183 days or less) OID

- Broker proceeds

- Bank deposit interest

- Proceeds from a wager placed by a nonresident alien individual in the games of baccarat, blackjack, craps, roulette, or big-6 wheel

- Foreign source dividends, interest, rents, or royalties

You still will have to file Form W-8BEN to obtain an exemption from US back-up withholding and information reporting for certain types of US source income.

How Deskera Can Assist You?

Deskera People allows you to conveniently manage leave, attendance, payroll, and other expenses. Generating pay slips for your employees is now easy as the platform also digitizes and automates HR processes.

Final Takeaways

This extensive guide has now come to a close. Now, for your future reference, we've created a summary of significant elements from this guide. Let's get started:

- W-8BEN or W8 forms are Internal Revenue Service (IRS) paperwork used by foreign firms and non-resident aliens (NRAs) to authenticate their country of residency for tax purposes, verifying that they claim for a lower tax rate withholding.

- W-8 forms are issued by the IRS. However, they are only delivered to withholding agents or payers, not to the IRS.

- To assure that your company is in compliance, you must request a filled Form W-8BEN from a foreign contractor.

- If you recruited someone from another nation to conduct services for your firm. Then, you don’t have to particularly send them the form 1099 at the end of the year

- Form W-8BEN should only be used by non-US citizens. Forms W-9, W-4, and others are filed by citizens of the United States.

- It's critical to complete the form as quickly as possible because the treaty prohibits you from being taxed twice (once by the US government and again by your home government).

- The contractor must not send the paperwork to the IRS once it is completed. The form should instead be delivered to you, the employer. Remind your contractor that the form includes sensitive information, so make sure you deliver it safely

- If circumstances change and the records on the form become inaccurate, a new form must be completed within 30 days. A change of circumstances could be a move to the United States or to another foreign country.

- The W-8BEN-E form is used by foreign entities claiming foreign status or tax treaty benefits

- Earners of qualifying income must take out Form W-8BEN to establish a claim for tax treaty advantages under the Internal Revenue Code. The Internal Revenue Service's website has a complete list of treaty countries.

- A Form W-8BEN is generally valid for three years. It further commences on the date it is signed and ends on the last day of the third calendar year once it's been completed

Related Articles